Children account for over 25% of all ATV injuries in the United States, and the average injured rider is just 12 years old. That number alone should stop any parent in their tracks. Yet thousands of families send their kids out on ATVs every weekend without a single dollar of insurance coverage, assuming it’s either unnecessary or too expensive. This guide is here to change that thinking. We’ll walk you through what youth ATV insurance actually is, when it’s legally required, what it covers, how much it costs, and how to find affordable options that keep your child protected and your family’s finances secure.

Table of Contents

- What is youth ATV insurance?

- Is ATV insurance required for youth riders?

- What does youth ATV insurance cover?

- How much does youth ATV insurance cost?

- Best practices for parents: Safety, compliance, and savings

- Our take: Why youth ATV insurance is non-negotiable

- Find the right ATV and protection for your family

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Essential protection | Youth ATV insurance shields your child and family from costly risks even if not legally required. |

| Coverage varies by state | Local laws may require insurance for public land, but private use still involves liability. |

| Cost-saving strategies | Combine liability-only policies, safety courses, discounts, and bundling to save up to 40%. |

| Age and training matter | Operator age and completion of safety training often determine eligibility and lower premiums. |

| Safe riding is key | Committing to safety practices and compliance ensures both coverage and your child’s well-being. |

What is youth ATV insurance?

Now that you understand the stakes, it’s important to know exactly what youth ATV insurance is and whom it’s designed for.

Youth ATV insurance refers to policies covering ATVs operated by or for minors under 16, typically purchased by parents as the named policyholder. It’s a specialty form of powersports insurance, meaning it’s built specifically for off-road vehicles rather than street cars or trucks. Standard auto insurance won’t cover your child’s ATV. Neither will most homeowner policies. Youth ATV insurance fills that gap.

The core purpose is twofold: protect your child from the financial consequences of an accident and protect your family from liability if someone else gets hurt. Think of it as your child’s safety net on the trail, just as essential as a helmet.

Here’s who this type of insurance is typically designed for:

- Minor riders under 16 who operate ATVs on private property, family land, or designated youth trails

- Parents or legal guardians who serve as the named policyholder and take on legal responsibility

- Youth ATV clubs and organized riding groups where liability exposure is higher

- Families who ride together on recreational outings, campgrounds, or off-road parks

Youth ATV insurance differs from standard ATV insurance in a few key ways. Standard policies often assume the operator is a licensed adult. Youth policies, by contrast, are structured around parental oversight and may include specific operator restrictions tied to age and supervision requirements. If you’re shopping for your child’s first machine, our youth ATV safe guide is a great place to start, and the Mini Sport Kids ATV is one of our most popular insurance-friendly choices for young riders.

Is ATV insurance required for youth riders?

Understanding the definition is just the start. Parents also need to know when youth ATV insurance is required and why regulatory details matter.

ATV insurance isn’t federally required in the United States, but state and local rules vary widely, and the gaps can catch families off guard. Some states mandate liability coverage for any ATV used on public land or trails. Others leave it entirely up to the rider.

Here’s a quick look at how requirements differ across a few key jurisdictions:

| Location | Requirement |

|---|---|

| Federal (USA) | No mandatory insurance |

| North Dakota | Liability insurance required |

| Saskatchewan (Canada) | Minimum $200,000 liability required |

| Most U.S. public lands | Proof of insurance often required |

| Private property (USA) | Not legally required, but liability risk remains |

Even when insurance isn’t legally required, the liability exposure on private land is real. If a neighbor’s child gets hurt on your property while riding your kid’s ATV, you could face a lawsuit that drains your savings. That’s a risk no family should take lightly.

Many youth ATV safety laws also tie into insurance eligibility, meaning that failing to follow age and helmet rules could affect your ability to file a claim.

Pro Tip: Even if your state doesn’t require insurance, call your local off-road park or trail system before your next ride. Many require proof of liability coverage at the gate, and showing up without it means your child sits out.

For a deeper look at how regulations affect young riders, our guide on ATV safety for kids breaks down what parents need to know state by state.

What does youth ATV insurance cover?

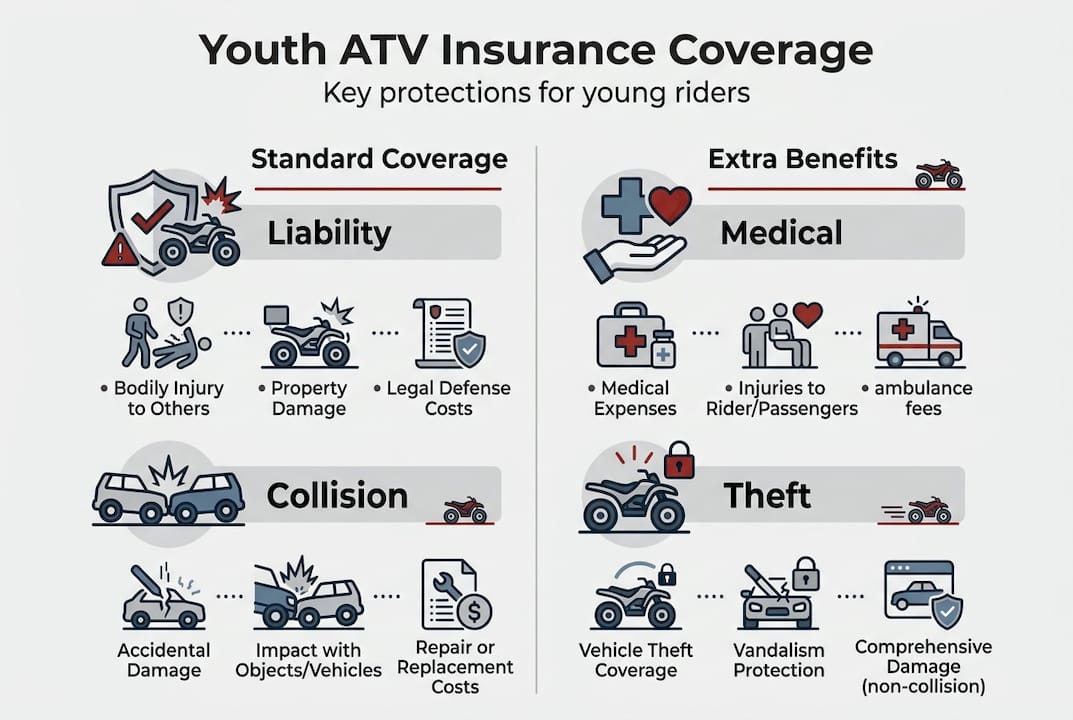

With requirements in mind, let’s look at what these policies actually provide in terms of financial and legal protection.

Most youth ATV insurance policies offer several core coverage types. Understanding each one helps you build a policy that fits your family’s real needs.

| Coverage type | What it pays for |

|---|---|

| Liability | Injuries or property damage your child causes to others |

| Collision | Repairs to your child’s ATV after a crash |

| Comprehensive | Theft, fire, weather damage, and non-collision events |

| Medical payments | Your child’s medical bills after an accident |

| Uninsured motorist | Protection if another rider has no insurance |

Here’s what can void your coverage entirely:

- Underage operation without supervision, especially if your policy requires parental oversight

- Unauthorized modifications to the ATV’s engine or frame that weren’t disclosed to the insurer

- Commercial or rental use of the vehicle, which falls outside recreational policy terms

- Riding on prohibited land, such as highways or restricted public areas

Age and operator restrictions are a critical detail. Youth riders face age restrictions, and many policies require operators to be at least 16 with a valid license for full coverage to apply. For younger children, parental supervision requirements are often written directly into the policy language. Ignoring these terms is one of the most common reasons claims get denied.

Some ATV policy exclusions also apply to accessories and modifications, so ask your insurer about add-ons for special equipment, custom parts, and towing or transport coverage if your family hauls the ATV to trails regularly.

Our guides on ATV safety essentials and parent safety tips can help you understand what behaviors keep coverage intact.

How much does youth ATV insurance cost?

Knowing what youth ATV insurance covers, you might wonder how affordable it can be. Let’s break down typical costs and how to save.

The good news: youth ATV insurance is genuinely affordable for most families. Premiums average $84 to $327 per year, with liability-only coverage starting around $99 annually. That’s less than $10 a month for basic protection. Full coverage with collision and comprehensive costs more, but it’s still a fraction of what a single emergency room visit or lawsuit could cost.

Several factors affect your premium:

- The ATV’s engine size and value: Larger, more powerful machines cost more to insure

- Your child’s riding experience: Newer riders may carry a higher risk rating

- Where you ride: Public trails and parks can raise your rate compared to private property

- Your deductible choice: A higher deductible lowers your monthly cost but increases out-of-pocket expenses after a claim

- Your location: State regulations and local claim rates influence pricing

Here’s how to bring that cost down without sacrificing protection:

- Enroll your child in a certified safety course. Many insurers offer discounts of 5 to 15% for completing an approved ATV training program.

- Bundle your ATV policy with your home or auto insurance. Bundling can cut total costs by 10 to 40%.

- Insure multiple vehicles under one policy. Multi-vehicle discounts apply if your family owns more than one ATV or powersports vehicle.

- Store the ATV securely. Locked garages or storage units reduce theft risk and can lower your comprehensive premium.

- Review your coverage annually. As your child grows and gains experience, your risk profile may improve and your rate may drop.

Pro Tip: Ask your insurer specifically about youth rider discounts. Not all companies advertise them upfront, but many will apply a discount if you ask and can show proof of safety training.

Our ATV buying checklist also covers how to choose a machine that’s easier and cheaper to insure from day one.

Best practices for parents: Safety, compliance, and savings

Beyond cost-saving, the right habits can keep your family safe and ensure you get all the benefits your insurance offers.

Children under 16 must follow special training and helmet rules in many states, and failing to comply doesn’t just create legal risk. It can invalidate your insurance claim when you need it most. Compliance and safety aren’t separate goals. They work together.

Here’s a practical checklist to maximize your coverage and minimize risk:

- Register your child’s ATV with your state or local authority if required, and keep the paperwork current.

- Document every ride. Note where your child rode, who supervised, and what safety gear was worn. This documentation supports claims.

- Enforce helmet use every time. Many policies require it, and it’s the single most effective injury prevention tool available.

- Complete a certified ATV safety course together as a family. The ATV Safety Institute offers youth-specific programs nationwide.

- Review your policy annually and update it when your child’s age, riding habits, or equipment changes.

- Notify your insurer of any ATV modifications before they’re made. Undisclosed changes are a leading cause of denied claims.

“The best insurance claim is the one you never have to file. Supervision, training, and the right gear are your first line of defense.”

Pro Tip: Keep a photo log of your child’s ATV condition before and after each season. If damage occurs, you’ll have clear before-and-after evidence to support your claim.

We’ve put together a guide on entry-level ATVs for kids that pairs well with these safety habits, helping you choose a machine that supports compliance from the start.

Our take: Why youth ATV insurance is non-negotiable

After exploring the technical and legal aspects, here’s our honest take based on real experiences in the powersports community.

We’ve seen it happen more times than we’d like. A family buys their child a great ATV, rides safely all season, and then one afternoon something goes wrong. A friend visiting the property gets hurt. The ATV rolls on uneven terrain. A neighbor’s fence gets clipped. And suddenly, a fun weekend turns into a five-figure problem that no one planned for.

Most parents think of insurance as something you need on public trails. The truth is, experts strongly recommend coverage even on private land, because liability doesn’t stop at your property line. If someone gets hurt on your land, you can be held responsible regardless of where the law stands on mandatory insurance.

The patchwork of state rules makes this even more complicated. What’s optional in one state is mandatory in the next, and families who travel with their ATVs often don’t realize they’ve crossed into a jurisdiction with different requirements. Insurance cuts through that confusion and gives you consistent protection wherever the adventure takes you.

We also think of youth ATV insurance the same way we think about helmets. You wouldn’t let your child ride without one. Insurance is the financial equivalent of that helmet. It won’t prevent every accident, but it will keep one bad day from becoming a financial crisis. Our comparison of ATV vs mini bike safety digs into how vehicle choice also plays into your overall risk picture.

Find the right ATV and protection for your family

Ready to take the next step? Start with the right ATV and complete your family’s safety plan.

At GoKarts USA, we believe every young rider deserves the thrill of adventure backed by real protection. Our lineup of youth-friendly machines, including the popular Mini Sport Kids ATV, is built with safety features and engine sizes that make them easier to insure and safer to ride. We’re not just here to sell you a vehicle. We’re your pit crew, your trail guides, and your fellow riders in this community. Pair the right machine with the right insurance policy, and you’ll send your child out on the trail with confidence every single time.

Explore our full catalog, take advantage of our current spring deals, and reach out to our team with any questions about choosing a youth ATV that fits your family’s needs and budget.

Frequently asked questions

Is youth ATV insurance mandatory in the United States?

Youth ATV insurance isn’t federally required, but some states and local parks may mandate proof of coverage, especially for public land use. Always check your state’s rules before heading out.

How much does youth ATV insurance typically cost?

Premiums typically range from $84 to $327 per year, with liability-only policies starting near $99 annually, making it one of the most affordable forms of powersports protection available.

Are there age limits for who can be covered by youth ATV insurance?

Yes, most policies cover minors under 16, and many require operators to be 16+ with a valid license for full coverage to apply. Younger riders typically need documented parental supervision.

Can taking a safety course lower my child’s ATV insurance premiums?

Absolutely. Safety courses often provide discounts of 5 to 15% on premiums, and some insurers require proof of training before issuing a youth policy at all.

Does my homeowner’s insurance automatically cover my child’s ATV?

Usually not. Most homeowner policies exclude ATV-related accidents, which is exactly why specialty youth ATV insurance is strongly recommended for any family with a young rider.